Article

What Makes a Good Target Company – Criteria and Red Flags

Selecting the right target company is one of the most important and, at the same time, most demanding steps on the path to a successful business acquisition. Anyone who approaches this decision impulsively or purely on gut instinct risks not only financial losses, but also a significant investment of time and energy. The key principle is this: take sufficient time to define which businesses are genuinely worth considering for you – and why. Choosing the right industry is the first and most critical step in this process. A common mistake many buyers make is "falling in love" with an industry or business model that they find personally exciting or fascinating as a hobby – perhaps because they are music enthusiasts or have a passion for hospitality. However, an emotional connection to a subject is no guarantee of commercial success. Just because you enjoy music does not mean that a music shop represents an attractive investment. Professional buyers take a clear-headed approach to analysing market potential, the competitive landscape, and the business model – and do not allow personal preferences to cloud their judgement. Only once the industry and the fundamental business model align with your objectives, your capabilities, and the market environment does it make sense to examine individual target companies more closely. In the following, we outline what to look for, how to identify risks at an early stage, and why a structured scoring model can make all the difference.

Selecting the right target company is one of the most critical steps in any business acquisition – and one of the most demanding. Those who make hasty decisions here risk financial losses and unnecessary effort. Take the time to clearly define which companies are worth considering in the first place – and why. Choosing the right industry is the first key step. Many buyers make the mistake of "falling in love" with a business model they find personally exciting, perhaps through hobbies or personal interests. But emotion is not a success factor. Professional buyers take a clear-headed approach, analysing market potential, competition, and business models free from personal bias. Only when industry, business model, and your own objectives are well aligned does it make sense to examine individual companies in greater depth.

1. Quantitative Criteria: The Hard Facts

Quantitative metrics form the basis of every business valuation and enable an objective comparison of different target companies. Particularly relevant – though by no means exhaustive – are:

- EBIT: Earnings before interest and taxes – this is one of the key metrics for assessing the operational performance of a business. Unlike EBITDA, EBIT also takes into account depreciation on tangible assets and amortisation of intangible assets. As a result, EBIT does not merely reflect pure operational earning power, but also provides insight into the capital intensity of the business and the wear and tear on its assets. A stable or growing EBIT indicates that the business is operating sustainably and profitably, achieving an attractive return even after accounting for the ongoing depreciation of machinery, equipment, or intangible assets such as licences or patents. Comparing EBIT margins against industry benchmarks is particularly useful for identifying strengths or weaknesses in the business model.

- EBITDA: The operating result before interest, taxes, and depreciation provides a realistic picture of the actual earning power – independent of accounting and financing structures.

- Revenue: A consistent, ideally growing revenue level demonstrates market demand and stability.

- Customer structure: A broad, diversified customer base reduces concentration risk.

- Growth rates: Historical and projected growth figures illustrate the company's potential and momentum.

2. Qualitative Factors: The Soft, Yet Decisive Criteria

Numbers alone are not enough for a well-founded decision. Qualitative factors are at least equally important, and often have a decisive influence on long-term success. These include, among others:

- Growth potential: Are there realistic opportunities for expansion, innovation, or new markets?

- Market positioning: How does the company stand in relation to its competitors? Are there sustainable unique selling points?

- Processes & Systems: Are structures and workflows scalable and digitalised?

- Dependencies: Is there a (too) great dependency on key individuals, suppliers, or technologies?

- Company culture: Do the values, management style, and team structure align with your own vision and goals?

Many of these criteria are already part of a professional search strategy – for more details, see the article Search Strategies and Market Approach in Business Acquisitions.

3. Positive and Negative Indicators

To give you a quick overview, we have compiled the most important positive and negative indicators (red flags).

Positive indicators (Top 10 – no particular order):

- Continuously growing revenue and, above all, profit

- Diversified, stable client base

- Experienced, committed second-tier management

- Clear unique selling points (USPs)

- Scalable processes and IT systems

- Innovation and adaptability

- Transparent, traceable figures

- Positive company culture and low staff turnover

- Clear expansion strategy

- Low legal and regulatory risks

Negative indicators (Red Flags, Top 10 – in no particular order):

- Dependency on individual customers (>30% of revenue)

- Non-transparent accounting or "creative" bookkeeping

- High employee turnover

- Outdated IT systems and processes

- Ageing or departing key personnel

- Pending legal disputes or unresolved liability issues

- Declining revenues or profits

- Lack of innovation capability

- No clear expansion opportunities

- Excessive debt or liquidity problems

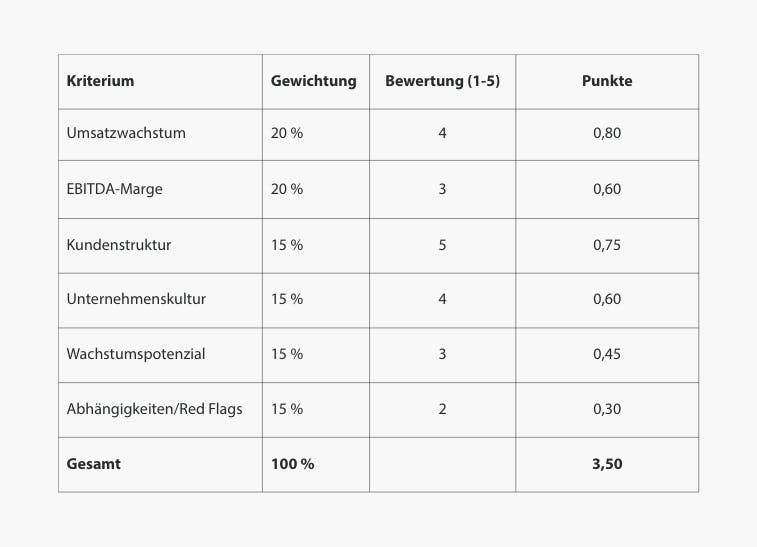

4. Evaluation Using a Scoring Model

To evaluate the wide range of criteria in a systematic and comparable way, using a scoring model is highly recommended. Each criterion is assigned a weighting and a score (1–5 points), and the combined total provides an overall picture of the target company's attractiveness. This allows for a more objective comparison of different businesses and helps identify potential red flags at an early stage.

Example of a simplified scoring model

The resulting values remain subjective; however, the model helps to consciously incorporate objective criteria. It also makes it easier to compare multiple options with one another.

Conclusion

Choosing the right target company is a balancing act between hard numbers, people, and potential. Do not let personal preferences or emotional motives guide you; instead, evaluate companies in a structured, objective, and professionally detached manner. A tried-and-tested scoring model and the consistent application of positive and negative indicators are effective methods for ensuring that objective criteria are deliberately factored into your decision. Once the target company has been selected, the next step is legal review – find out more in Transactions and Legal Due Diligence.

You will find a complete overview of all steps in our business acquisition checklist.